What Are the Outlook and Challenges for Cryptocurrencies and Blockchain for Finance and Investment Banks

As in all areas of public and corporate life, the digital transition that began at the end of the 20th century has led to structural changes in the banking world.

This transition, initially marked by the disruption caused by the large-scale development and high-speed growth of fixed and mobile internet capacities, is far from complete. Many technological innovations, that are currently more or less mature, are likely to lead to new (r)evolutions in the near future, with a significant impact on different areas of the banking world's activity, whether it is in terms of products managed, marketing methods or processes.

Among these technological developments, those based on blockchain, and the development of artificial intelligence (AI) probably have the greatest potential for disruption. However, recent developments in these two technologies have contrasted, to say the least. While the conversational AI tool ChatGPT, the first to give the public a concrete vision of the power of this technology, has given AI a global and generally positive buzz, blockchain in general, and its most popular use - cryptocurrencies - in particular, have seen their image tarnished by the series of scandals involving certain players in the crypto ecosystem in the second half of 2022.

In this context, the aim will be to focus on technologies based on blockchains, and to try to make the link between recent events and their impact on the potential uses that could be made of them in the banking world and, more generally, to take stock of the initiatives being made by various players (commercial banks, central banks, clearers/custodians, etc.) to deploy these technologies in the fields of banking, insurance and financial services.

Blockchain and Cryptocurrencies: Major Product Families and Ecosystem Players

In recent months, the crypto ecosystem described above has experienced several upheavals, with major consequences for the credibility of these new types of assets and the various players associated with them:

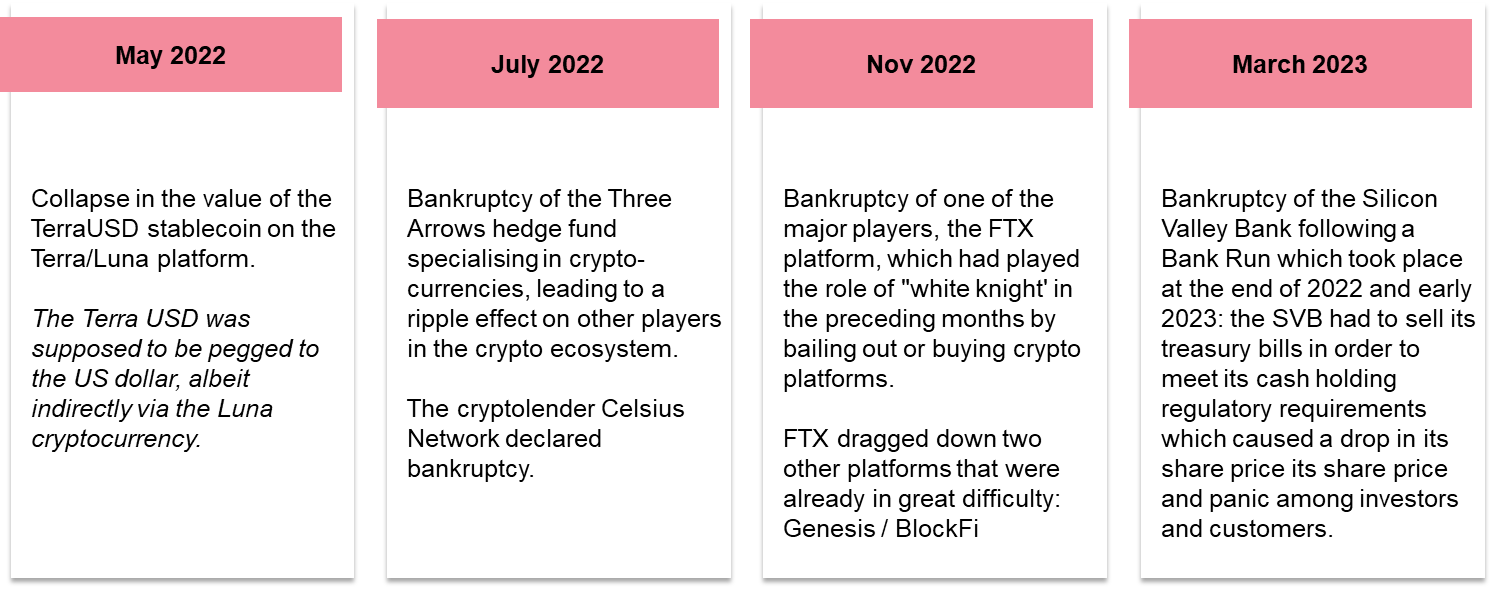

- Volatility of cryptocurrency prices: the Covid crisis was characterised, after the initial shock of spring 2020, by a period of euphoria on the financial markets, somewhat paradoxical in absolute terms but explainable. On the economic front, on one hand, this was due to the deployment of accommodating monetary policies by the various central banks aimed at preserving the stability of economic and financial systems and secondly, by the prospects of an end to the crisis that emerged at the end of 2020, notably following the initial publication of very encouraging results from various Covid vaccines. The cryptocurrencies have been no exception, enjoying an even more significant upturn than that of traditional financial assets. For instance, the Bitcoin price rose from around USD 7,000 in early 2020 to almost USD 65,000 by the end of 2021. The "bear market", which took hold of all financial markets in 2022 following the very rapid implementation of major monetary tightening by central banks in order to deal with the inflationary crisis was also reflected in the price of cryptocurrencies with Bitcoin, for example losing almost 70% of its value in the first half of 2022, before stabilising at around USD 20,000. This extreme volatility has damaged the positive image of cryptocurrencies, far from the idea of a safe haven that some players were trying to popularise. Today, crypto currencies are more often seen as highly speculative instruments more or less similar to the various "meme stocks" that made the news at the height of the stock market euphoria.

- In recent months, in addition to this high volatility, there have been a number of high-profile scandals in the crypto news which have helped to create a climate of mistrust towards cryptocurrencies and the crypto ecosystem in general.

A few months were enough for a large part of the crypto ecosystem to fold and reveal several frauds, together with the fact that a large number of the activities conducted by crypto players involved disproportionate risks and could not therefore be viable in the long run.

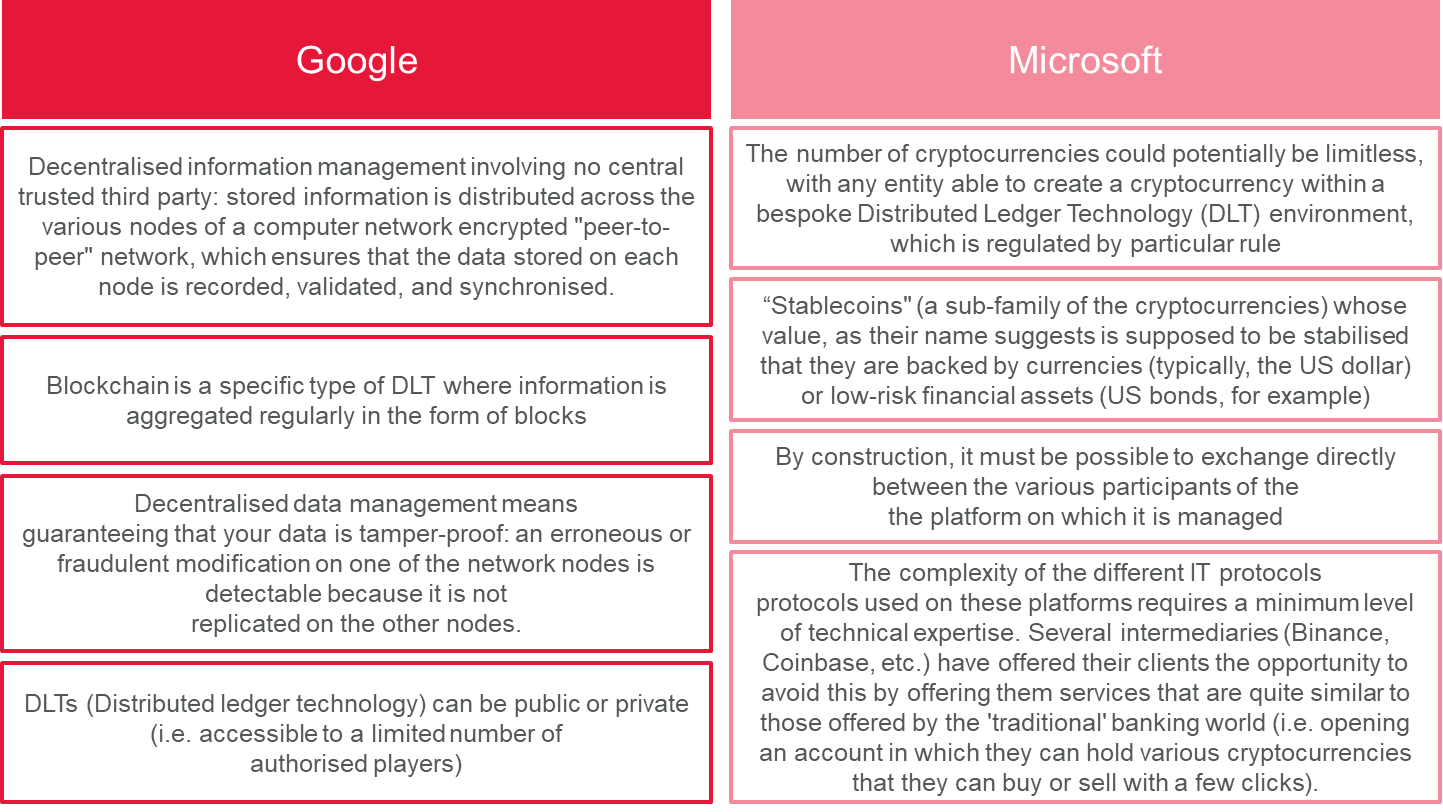

It is important to note however that while the collapse of the stablecoin TerraUSD also exposed flaws in DLT/Blockchain technologies, the underlying DLT technology remains itself reliable.

With not a single case of accusation or piracy after more than 10 years of operation, it is more the use that has been made of cryptocurrencies and DLT/blockchain technologies by innovative players that are being questioned. Indeed, the growing technological possibilities have sparked interest, with the creation of many FinTechs and other unicorns, which have had varying life spans. These innovations have created an effect similar to that of a bubble around the crypto ecosystem.

A bubble with blurred edges, because regulation hasn't kept up with the pace of change, leaving the field open to opportunistic and/or immature players.

The Financial Sector Under Pressure to Adapt

In this context regulators in a large number of countries (including the United States, Europe and the United Kingdom) have unsurprisingly announced plans to speed up the implementation of enhanced regulations for the crypto ecosystem, with the aim of bringing them closer to those of the traditional banking world (the latter aiming in particular to circumscribe the principal causes of the systemic crisis that affected the crypto ecosystem: uncontrolled use of customer deposits, failure to take counterparty risk into account, price manipulation, etc.).

These regulations, and in particular the European regulation MiCA, which is expected to come into force in 2024, should provide a strong framework for the issuance, custody, trading and marketing of crypto-currencies, with players in the ecosystem required to be licensed by the regulator and to be authorised by the regulator and to implement KYC and anti-money laundering procedures similar to those of the banking world.

In addition, the Basel Committee has ruled on the prudential treatment to be applied to this type of asset. While no additional capital requirements will be imposed on banks responsible only for the custody of crypto assets belonging to their customers, the same does not apply on shares which they own.

In fact, two categories of crypto assets have been established, on one hand security tokens and stablecoins, on the other native cryptos such as Bitcoin and Ether. The latter, if held by a bank, has a significant prudential impact - a capital equivalent to 100% of the value of the crypto assets must be held in reserve. Furthermore, banks will have to limit their exposure to this type of crypto asset to a maximum of 2% of their capital.

Given the battered image of cryptocurrencies, and pending the implementation of these new regulations which should lead to a shakeout of the players and the 10,000 odd crypto-currencies identified in mid-2022. Banks that were considering developing cryptocurrency-related activities (spot and derivative trading, launch of ETFs or structured products based on crypto-currencies, etc.) have shelved, put on hold, or even abandoned them in order to assess and control the related risks, both in terms of image and reputation. For banks, it is therefore urgent to wait before considering or reconsidering this type of activity, at least until the new regulations comes into force and the crypto ecosystem is cleaned up and clarified.

While cryptocurrencies are no longer, at least in the short run, a major area of development for banks, two technological development projects with certain characteristics similar to those of cryptocurrencies are currently being studied and could have a significant impact on the way they conduct their business.

The Development of Digital Currencies by Central Bank

“CENTRAL BANK DIGITAL CURRENCY (CBDC)”

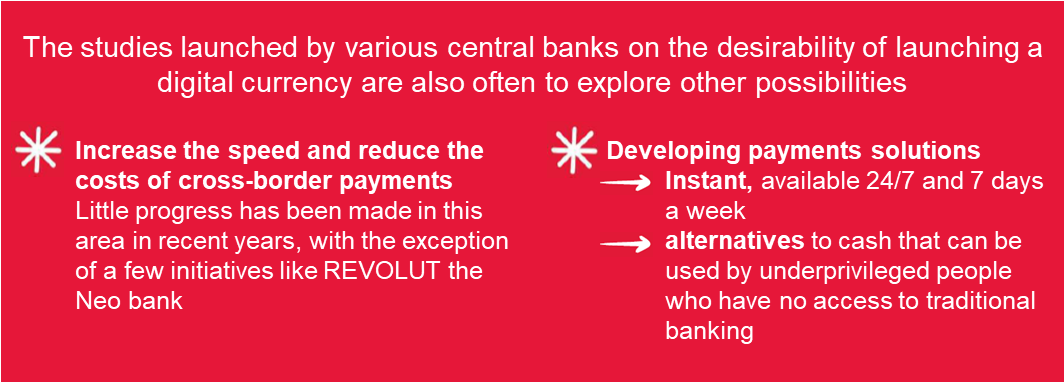

The reasons that have led central banks around the world to consider this type of project are varied and it is not always easy to discern which of the official reasons cited were the main drivers behind the launch of this type of project. However, we can imagine that the emergence and popularisation of cryptocurrencies in the 2010s have been identified as risk factors by central banks insofar as these cryptocurrencies could gradually replace official currencies for making payments.

In addition, beyond the most popular cryptocurrencies such as Bitcoin and Ether, projects and ideas launched by internet giants in order to create cryptocurrencies that can be used to carry out transactions on their platforms (such as Facebook's 'Libra' digital currency project by Facebook/Meta) could also be perceived as, in the event of mass adoption by users of these platforms, real threats that could eventually lead to the marginalisation of the use of official currencies, at least online. One can also imagine that from the moment a central bank has started thinking about introducing a digital currency, the other central banks felt more or less obliged to study the subject as well in order to avoid the risk of being left without a solution in the event that a central bank's CBDC becomes successful beyond its borders and a significant means of payment in other countries.

The level of maturity of studies and projects launched on the subject by central banks vary considerably, there are currently 11 CBDCs in operation, 17 that are in the pilot phase, and some sixty that are in development or research phase (source: Atlantic Council). The technological solutions implemented for operational CBDCs or envisaged in current studies and projects are diverse, ranging from DLT blockchain (e.g. permissioned DLT - accessible to a limited number of authorised participants - for the e-Naira in Nigeria) to more traditional or hybrid solutions.

In Europe, an initial report on the advisability of launching a digital euro was published under the aegis of the ECB in October 2020 and a study phase was formally launched in 2021 with the aim of defining its priority functionalities and uses. The conclusions of this study should be presented to the Governing Council of the ECB in autumn 2023, at which point it will then decide whether to launch the project to development the digital euro.

The latest interim report published in December 2022 by the group of experts in charge of this study suggests that the direction that will be recommended in terms of the uses, if any, of this digitised version of the euro will focus on payments and exchanges by retail users, for example making payments in physical shops and online as well as the possibility of exchanging digital euros offline as an alternative to cash payments. In January 2023, the Governor of the Banque de France announced clear intentions of the ECB to adopt these Blockchain/DLT technologies with a view to tokenisation of both wholesale and retail activities.

In terms of the underlying technology the choices are not yet very clear, but the ECB Governing Council has agreed that the study should focus on the following types of solution for instance, for in-store or online payments, an architecture including validation of transactions by a third party (commercial bank or payment services provider) and the use of a private or permissioned DLT/blockchain. would be considered.

However, this has not yet clarified the impact of this direction on the rest of the banking ecosystem. With such extensive decentralisation of data and transaction management how can key control processes such as KYC and compliance or AML, be implemented?

The same applies to use of this CBDC for retail purposes and the definition of restrictions on the sums that can be kept in digital euros. Indeed, a maximum amount held per person and/or the provision of negative interest rates applicable to amounts held above certain thresholds would make it possible to avoid a significant reduction to liquidity deposits in bank accounts, thereby limiting the repercussions on the banks' ability to fulfil their role in financing the economy.

In addition, the ability to hold unlimited amounts of digital euros could facilitate bank runs in the event of a crisis, by enabling the instant transfer to digital euros of assets deposited in bank accounts.

Implementation of DLT / Blockchain Infrastructures for Post-Trade Operations

In addition to currencies, securities are another segment of the financial world where studies on the deployment of blockchain technologies are multiplying.

The aim here is to manage financial instruments on this type of platform in the form of tokens or smart contracts, in order to simplify the complex validation and matching processes that are currently used in the back office to ensure back-office processes for issuing and settling securities and as well as OST. In particular, the standard settlement time on most financial markets is of T+2, which creates execution risk requiring the implementation of margin calls, which represent a significant cost for key players in the financial markets.

Several tests have been carried out in recent years to validate the possibility of managing the issuance and securities via DLTs/blockchains. For example, Forge, a subsidiary of the Société Générale group specialising in in crypto assets, issued a covered bond on a blockchain in 2020 and, in 2021, took part, along with other players, in the issuance by the European Investment Bank (EIB) of a tokenised bond settled on a public blockchain against a CBDC issued on an experimental basis by the Banque de France. In November 2022, the EIB issued a second digital bond, this time on a private blockchain, with same day settlement and listing on the Luxembourg Stock Exchange.

A test involving several players (including the Banque de France and the Agence France Trésor) and covering a wide range of functionalities was also carried out in October 2021 via an authorised blockchain and validated the feasibility and effectiveness of this technology in the processing of a tokenised OAT issue, which was also settled against an experimental CBDC issued by the Banque de France. In addition to the initial issue and distribution to the participating primary dealers (BNPP, Société Générale, Crédit Agricole and HSBC), secondary sales/purchases, repo and auto-collateralisation transactions, coupon payments and failed settlement management tests were also undertaken. Settlements were carried out with very positive results pointing to a promising outlook for reducing the costs and lead times of the various processes studied.

Although they are often still in the experimental stages, the various CBDC and tokenisation projects for financial assets represent a major development likely to generate new uses and functionalities, as well as profound upheavals in the processes implemented in the world of financial services and markets.

However, in order to have a complete and balanced view of the benefits and potential risks that could be associated with the deployment of these developments, a number of points of attention should also be highlighted. As far as the tokenisation of financial instruments is concerned, we can point out that several projects aimed at implementing blockchain infrastructures for managing post-trade processes have recently been abandoned after it was found that they were not technically and/or financially viable.

-

We.trade, a project led by a consortium of 12 banks and aimed at implementing a private blockchain-type system for certain trade finance services, was halted in June 2022.

-

In July 2022, it was B3i's turn to declare bankruptcy and cease operations - this project, led by a group of 15 insurance and reinsurance companies, aimed to develop a solution for optimising the premium payment and reimbursement processes associated with insurance contracts by using smart contracts managed on a blockchain.

-

Finally, in November 2022 ASX Settlement, the entity responsible for securities traded on the Australian stock exchange (ASX) announced (after 7 years of development and more than 150 million euros of expenditure) that it was halting a project for a blockchain-based clearing platform.

While no generic conclusions should be drawn from these failures, they nonetheless demonstrate the issues that can arise when deploying a new technology to replace an infrastructure that may be technically outdated, but which generally provide robust support for the complex processes involved in back-office involving numerous players, very large volumes and the management of a wide variety of data types and a wide variety of transaction types. Even more so than for other types of projects, an accurate assessment of the DLT/blockchain platform to manage and validate post-trade processing and processes in a test environment will therefore be essential before any large-scale deployment of these technologies.

Toward the Digital Euro

To return more specifically to the eurozone, one point of attention concerns the potential impact of the choices that will be made in terms of designing a digital euro on the DLT/Blockchain projects designed for post-trade activities, as the various experiments and tests carried out to date in Europe have most often been on platforms that include a CBDC (generally provided on an experimental basis) by the Banque de France), for use in retail payments, it would then be necessary to think about the impacts of a tokenised mode on the operating principles

Furthermore, the business model and uses currently envisaged by the ECB for a digital euro will have to take into account that some of the reasons which led to the feasibility study for creating a digital euro are no longer actual, since the first report on this subject was published in October 2020, for example:

-

The risk of cryptocurrencies and stablecoins taking a significant share of the European payments market, to the detriment of the euro.

-

The various characteristics mentioned in the first part of this document (extreme volatility, fraud, etc.), this risk can now be seen as much more remote than it was in 2020, even more so as the use of cryptocurrencies/stablecoins to make payments (particularly of small amounts) never seemed to take off, even before the crisis of 2022.

-

Additionally, the Internet giants' cryptocurrency projects and plans are now more discreet or have even been abandoned, this is notably the case for Facebook/Meta, which has abandoned Libra (since renamed Diem).

-

Finally, following the Covid crisis the acceptance by physical shops of bankcard payments for small (or even very small) amounts has grown considerably, which in turn is likely to reduce the potential interest in the digital euro as an alternative to cash in the Eurozone, where bank penetration is very high.

While the various drawbacks mentioned above call for a cautious approach to the various CBDC and tokenisation of financial assets projects currently underway, it is nonetheless reasonable to remain optimistic about the future. Indeed, the development of these new technologies will probably lead to concrete progress, directly or indirectly, in the banking and financial world in general.

-

Direct progress insofar as it is likely that these technologies will be able to find, in the relatively short term, applications that are particularly suited to specific financial activities.

-

Indirect progress insofar as the emergence of these technologies will, at the very least, act as a 'spur' by encouraging banks to move out of their comfort zones in certain areas where little progress has been made in terms of cost. In the same way that the Covid crisis made things, that previously seemed complicated to implement, possible in a very short space of time for example the increasingly widespread acceptance of payments (for smaller and smaller amounts), development of instant payments or improvements (in terms of cost or time) in the conditions under which cross-border payments are also possible, without a major technological revolution.

A pragmatic approach to these technological developments will ideally provide the best of both worlds by identifying the uses (existing or new) for which they offer significant added value, and those for which the improvements or innovations they enable are realisable by adapting existing technologies and infrastructure.

The road ahead is a winding one, as the introduction of a digital euro raises many questions that will need to be answered in order to structure the future market in a way that is optimal and secure for all of its users, traditional and innovative players, central and commercial banks, stakeholders and individuals.

For commercial banks in particular, the impact could be major, affecting both their roles and their local and global organisations, as well as the Target Operating Model of their businesses and the IT infrastructures that support them today.

Dislaimer: This article is co-written with Aurélie Demangeon – Director – Banking industry – CGI Business Consulting.

Trending

-

1 Building a Strong Financial Foundation: Saving, Investing, and Retirement Planning

Daniel Hall -

2 Franchise Investment Pitfalls to Avoid: A Beginner's Checklist

Daniel Hall -

3 Why Selling to an iBuyer Could Be the Best Move for Your Home

Daniel Hall -

4 Financial Tips for Businesses: Reducing Expenses Without Sacrificing Quality

Daniel Hall -

5 9 Tips to Help You Secure a Graduate Job in Finance

Daniel Hall

Comments